Thursday, January 31, 2008

ROI of a Vasectomy

Sorry folks, playing catch up from vacation. Will show you the pictures later. In the meantime here's a "Best of the Captain."

It was determined a while ago that Captain Capitalism would not sow his seed for despite high demand by the ladies, a little Jr. Captain Capitalism would wreak havoc upon my life and no doubt be turned to the Dark Side by the public schools requiring a kind of Obi Wan Kenobi versus Anakin Skywalker ultimate showdown in the end, where no doubt I would surely win for I am on the Good Side of the Force and he would be a product of the public schools.

Having said that, it was determined a while ago that Captain Capitalism would have a vasectomy and his friends in St. Paul got the brilliant idea of having a "Vasectomy Fund Raiser Party" where the theme was akin to "He doesn't want to breed, and the World doesn't want him breeding either! Save the World! Donate to Captain Capitalism's Vasectomy Fund!" Alas as the time nears, it got me thinking, "how much am I going to save by having this vasectomy?"

Or more specifically, "what kind of rate of return am I going to realize on a little snip-snip?"

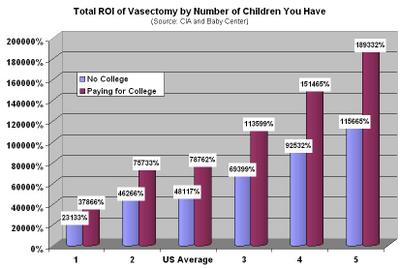

So with a little number crunching and research I figured that by plopping down $1,200 for the vasectomy, and assuming I would have had the 2.08 children that is the US average, I would save about $577,000 (or $945,000 if I was stupid enough to pay for my 2.08 childrens' way through college). This translates into a whopping total Return on Investment (ROI) of 48,177% (or 78,762%, respectively).

Of course, not everybody has 2.08 kids. Some are microscopically wiser only spitting out one. Others are complete morons producing 5 children and no doubt requiring me to subsidize them. Thus I calculated the total ROI's for varying levels of children as a handy dandy reference guide for those of you pondering having children;

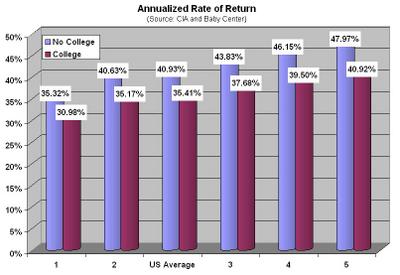

I also annualized these rates of return so that you may compare them against the performance of your 401k/403b funds, and even that of the seemingly "unbeatable" S&P 500 (and no, it's not a mathematical error that paying for college results in a lower annualized rate of return).

Look out Warren Buffett. There's a new sheriff in town.

It was determined a while ago that Captain Capitalism would not sow his seed for despite high demand by the ladies, a little Jr. Captain Capitalism would wreak havoc upon my life and no doubt be turned to the Dark Side by the public schools requiring a kind of Obi Wan Kenobi versus Anakin Skywalker ultimate showdown in the end, where no doubt I would surely win for I am on the Good Side of the Force and he would be a product of the public schools.

Having said that, it was determined a while ago that Captain Capitalism would have a vasectomy and his friends in St. Paul got the brilliant idea of having a "Vasectomy Fund Raiser Party" where the theme was akin to "He doesn't want to breed, and the World doesn't want him breeding either! Save the World! Donate to Captain Capitalism's Vasectomy Fund!" Alas as the time nears, it got me thinking, "how much am I going to save by having this vasectomy?"

Or more specifically, "what kind of rate of return am I going to realize on a little snip-snip?"

So with a little number crunching and research I figured that by plopping down $1,200 for the vasectomy, and assuming I would have had the 2.08 children that is the US average, I would save about $577,000 (or $945,000 if I was stupid enough to pay for my 2.08 childrens' way through college). This translates into a whopping total Return on Investment (ROI) of 48,177% (or 78,762%, respectively).

Of course, not everybody has 2.08 kids. Some are microscopically wiser only spitting out one. Others are complete morons producing 5 children and no doubt requiring me to subsidize them. Thus I calculated the total ROI's for varying levels of children as a handy dandy reference guide for those of you pondering having children;

I also annualized these rates of return so that you may compare them against the performance of your 401k/403b funds, and even that of the seemingly "unbeatable" S&P 500 (and no, it's not a mathematical error that paying for college results in a lower annualized rate of return).

Look out Warren Buffett. There's a new sheriff in town.

Tuesday, January 29, 2008

Rents Ultimately Drive Property Values

I love this chart. estimates that around 2012 in Irvine, CA (which is probably not as representative as the rest of the country) rents will catch up to the market value of the houses out there. Hat tip to another charting blogger.

Sunday, January 27, 2008

Go O

Again, not to scare all you fellow capitalists out there, I don't want Obama to win the presidency, but I am still cheering him on since he does represent a changing of the old guard.

Going to be a shame if we have to beat him in the presidential election. Would have so much preferred to destroy Hilary.

Going to be a shame if we have to beat him in the presidential election. Would have so much preferred to destroy Hilary.

Saturday, January 26, 2008

When I Am King

Someday I will have an office.

And someday I will be in such position of power, that I will not have one of these "motivational" posters;

But rather "de-motivational" posters like this one;

However, prominently displayed with a spotlight shinning on it before you walk into my office will be this one.

Hat tip to Mr. Ryan Fuller.

And someday I will be in such position of power, that I will not have one of these "motivational" posters;

But rather "de-motivational" posters like this one;

However, prominently displayed with a spotlight shinning on it before you walk into my office will be this one.

Hat tip to Mr. Ryan Fuller.

The 2 Cylinder Mustang Convertible

I am posting from Camp Verde, AZ. And the only reason, the SOLE ONLY REASON I PULLED OVER WAS IN HOPES THE GAS STATION WOULD HAVE INTERNET ACCESS SO I COULD SHARE THIS INGENIOUS IDEA I JUST HAD!

The 2 cylinder Ford Mustang!

Yes!

You see, I think there's a HUGE market for a 2 cylinder Ford Mustang. For while driving out of Phoenix, I've spent the past 2 hours getting behind no less than 30 of those new Ford Mustangs. And the reason I'm behind them is because they're always in the left lane, driving next to a semi-truck, going the exact same speed which is usually 5 miles per hour UNDER the speed limit.

Inevitably we hit a mountain and the SEMI-TRUCK usually pulls ahead of the Ford Mustang,, allowing me the chance to pass. And when you pass people who clog up the left lane, you almost have this biological urge to look over and see what they look like. As if you're going to see some physical ailment that would explain why they're such retards for driving 10 MPH below the speed limit in the left lane.

Half expecting to see a 12 year old child at the wheel, the only thing I visually noticed that was out of the 30 or so Mustangs I passed, 25 we're occupied by normal looking, gray-haired middle aged couples with big smiles on their face. Not because they were vindictive and knew they had held me and half of the northbound traffic out of Phoenix up for the past 8 hours, but because they were driving a really cool and sweet Ford Mustang and just enjoying the cruise on a beautiful day, completely ignorant of the Rule of the Left Lane.

And this is a tragedy. For I don't think that I saw one Mustang that was using all 6 or 8 of its cylinders. I did not see one Mustang even pushed to 1/2 of its performance limits. If I was in that car, I'd not be in Camp Verde, I'd be in Canada right now.

Thus, since it is obvious that the slightly elder generation wants to buy the classical looking Mustangs that have come out in the past year, but don't want an actual sports car, I recommend the Ford Motor Corporation develop the 2 cylinder Ford Mustang, because that's about all the cylinders they're going to need.

"Yes, the 2 cylinder Ford Mustang. It looks cool, but drives slow! Are you in no particular rush to be anywhere? Want to take up precious traffic space in the left lane? Looking to get great fuel efficiency, but absolutely no performance whatsoever? Then get the 2 Cylinder Ford Mustang! It just looks cool, but it's not!"

And for all of you folk that have already bought Mustangs with all those nasty cylinders, don't worry you can donate it me and the younger folk. We'll take them off your hands and drive them like they were intended to be driven.

Now I must go. I think in the past 30 minutes of typing and eating and fueling, the Mustang Caravan might be catching up to me.

The 2 cylinder Ford Mustang!

Yes!

You see, I think there's a HUGE market for a 2 cylinder Ford Mustang. For while driving out of Phoenix, I've spent the past 2 hours getting behind no less than 30 of those new Ford Mustangs. And the reason I'm behind them is because they're always in the left lane, driving next to a semi-truck, going the exact same speed which is usually 5 miles per hour UNDER the speed limit.

Inevitably we hit a mountain and the SEMI-TRUCK usually pulls ahead of the Ford Mustang,, allowing me the chance to pass. And when you pass people who clog up the left lane, you almost have this biological urge to look over and see what they look like. As if you're going to see some physical ailment that would explain why they're such retards for driving 10 MPH below the speed limit in the left lane.

Half expecting to see a 12 year old child at the wheel, the only thing I visually noticed that was out of the 30 or so Mustangs I passed, 25 we're occupied by normal looking, gray-haired middle aged couples with big smiles on their face. Not because they were vindictive and knew they had held me and half of the northbound traffic out of Phoenix up for the past 8 hours, but because they were driving a really cool and sweet Ford Mustang and just enjoying the cruise on a beautiful day, completely ignorant of the Rule of the Left Lane.

And this is a tragedy. For I don't think that I saw one Mustang that was using all 6 or 8 of its cylinders. I did not see one Mustang even pushed to 1/2 of its performance limits. If I was in that car, I'd not be in Camp Verde, I'd be in Canada right now.

Thus, since it is obvious that the slightly elder generation wants to buy the classical looking Mustangs that have come out in the past year, but don't want an actual sports car, I recommend the Ford Motor Corporation develop the 2 cylinder Ford Mustang, because that's about all the cylinders they're going to need.

"Yes, the 2 cylinder Ford Mustang. It looks cool, but drives slow! Are you in no particular rush to be anywhere? Want to take up precious traffic space in the left lane? Looking to get great fuel efficiency, but absolutely no performance whatsoever? Then get the 2 Cylinder Ford Mustang! It just looks cool, but it's not!"

And for all of you folk that have already bought Mustangs with all those nasty cylinders, don't worry you can donate it me and the younger folk. We'll take them off your hands and drive them like they were intended to be driven.

Now I must go. I think in the past 30 minutes of typing and eating and fueling, the Mustang Caravan might be catching up to me.

Friday, January 25, 2008

Why You Can't Argue with a Liberal

A liberal friend of mine (yes I have them) sent me this as she knows my affinity for charts.

And key to understanding this is that she is about 55 years old

The reason that this is key that any truly (and I mean this) independently thinking individual who is intellectually honest will look at each "item" and say, "wait a minute, that is..." fill in the blank.

"Fill in the blank"

Irrelevant

Not adjusted for inflation

Not adjusted for the size of the economy

Cherry picked data (my personal favorite is the 4 countries whose opinion of the US has dropped...OUT OF 176 FREAKING NATIONS IN THE ENTIRE WORLD!)

In anycase, long story short, for I am on vacation, it is the perfect example of why you really can't argue with a liberal beyond a certain age, because they have an ideology they're going to subscribe to and will find the data that FITS that ideology, never letting the data or fact actually form their ideology.

I know this chart will be frustrating because it is so disingenuous plus there are some outright lies (and I like how they cite their figures) but take solace in the fact that this is literally their "best" argument. Additionally, this should emphasize the importance of being intellectually honest. If you really do care about society and your fellow man, you wouldn't resort to such pathetic tricks and selective data when it comes to advocating how an entire nation should be governed.

Additionally, I might have said something to the extent that "Under President Washington income per capita was only $560. Wow, he sucks even worse than Bush."

Again, why you should leave the adjusting for inflation to the professionals.

And key to understanding this is that she is about 55 years old

The reason that this is key that any truly (and I mean this) independently thinking individual who is intellectually honest will look at each "item" and say, "wait a minute, that is..." fill in the blank.

"Fill in the blank"

Irrelevant

Not adjusted for inflation

Not adjusted for the size of the economy

Cherry picked data (my personal favorite is the 4 countries whose opinion of the US has dropped...OUT OF 176 FREAKING NATIONS IN THE ENTIRE WORLD!)

In anycase, long story short, for I am on vacation, it is the perfect example of why you really can't argue with a liberal beyond a certain age, because they have an ideology they're going to subscribe to and will find the data that FITS that ideology, never letting the data or fact actually form their ideology.

I know this chart will be frustrating because it is so disingenuous plus there are some outright lies (and I like how they cite their figures) but take solace in the fact that this is literally their "best" argument. Additionally, this should emphasize the importance of being intellectually honest. If you really do care about society and your fellow man, you wouldn't resort to such pathetic tricks and selective data when it comes to advocating how an entire nation should be governed.

Additionally, I might have said something to the extent that "Under President Washington income per capita was only $560. Wow, he sucks even worse than Bush."

Again, why you should leave the adjusting for inflation to the professionals.

Thursday, January 24, 2008

Cats are Not a Substitute for a Boyfriend

OK, look, ladies let me help you because I genuinely care to help. I do!

Cats are not cool.

No, I know you think they are. But in fact, they are not.

No, actually quite the contrary. Yale physicists and paleontologists trace the cats' evolutionary origins from Hell.

It's true, saw it on the Discovery Channel. Not making this up. Scouts honor.

Anyway, yes, cats are from Hell apparently and in reality they do not, repeat do NOT help you get a boyfriend. They actually plot AGAINST your getting a boyfriend, that's if they're not planning your death whilst you sleep. Worse still they actually deter you from getting a boyfriend ESPECIALLY WHEN YOU'VE BECOME SO ACCUSTOMED TO THEM THAT YOU LET THEIR STENCH AND ODOR FERMENT IN YOUR APARTMENT, INFUSING ITSELF INTO THE WALLS SO WHEN PEOPLE FROM THE OUTSIDE COME IN AND TAKE ONE WHIFF THEY DIE!!!

And it's not a stark, chemically, skunk smell. No, it's a biological, cat urine, 6 month old kitty liter smell. That the biological remnants of whatever cause cat stench is taking on a new, merged, mutated life form with improved odor.

Also, most people have an allergy to cats. So, you know, maybe vacuum the 3 inches of cat hair that has accumulated on your couch? And it would help that instead of 7 cats, you know you just get one? The American Dental Association says 4 out of 5 dentists prefer less cats. So, you know, there you go.

Anyway, only reason I bring this up is because a good friend of mine has decided to let me crash at her joint whilst I vacation here in Arizona (for I am an economist and it is cheaper to house sit than to pay for a hotel). And the truth is her cats are not that bad nor is her hygiene habits in cleaning up after them. However, as I house sit for three cats the smell has triggered memories I tried to forget long ago.

Just doing a public service announcement.

Cats are not cool.

No, I know you think they are. But in fact, they are not.

No, actually quite the contrary. Yale physicists and paleontologists trace the cats' evolutionary origins from Hell.

It's true, saw it on the Discovery Channel. Not making this up. Scouts honor.

Anyway, yes, cats are from Hell apparently and in reality they do not, repeat do NOT help you get a boyfriend. They actually plot AGAINST your getting a boyfriend, that's if they're not planning your death whilst you sleep. Worse still they actually deter you from getting a boyfriend ESPECIALLY WHEN YOU'VE BECOME SO ACCUSTOMED TO THEM THAT YOU LET THEIR STENCH AND ODOR FERMENT IN YOUR APARTMENT, INFUSING ITSELF INTO THE WALLS SO WHEN PEOPLE FROM THE OUTSIDE COME IN AND TAKE ONE WHIFF THEY DIE!!!

And it's not a stark, chemically, skunk smell. No, it's a biological, cat urine, 6 month old kitty liter smell. That the biological remnants of whatever cause cat stench is taking on a new, merged, mutated life form with improved odor.

Also, most people have an allergy to cats. So, you know, maybe vacuum the 3 inches of cat hair that has accumulated on your couch? And it would help that instead of 7 cats, you know you just get one? The American Dental Association says 4 out of 5 dentists prefer less cats. So, you know, there you go.

Anyway, only reason I bring this up is because a good friend of mine has decided to let me crash at her joint whilst I vacation here in Arizona (for I am an economist and it is cheaper to house sit than to pay for a hotel). And the truth is her cats are not that bad nor is her hygiene habits in cleaning up after them. However, as I house sit for three cats the smell has triggered memories I tried to forget long ago.

Just doing a public service announcement.

Wednesday, January 23, 2008

Blowing Up Satellites

Hello all Junior, Deputy, Official and otherwise Aspiring Economists!

The Captain is on vacation and will not be making lot's of posts as I'm hiking out in the wilderness and sleeping at waysides (as hotels cost money, and it is more economical). Plus I'm out in Arizona and this is a big state with a lot of open spaces where there is no internet access.

Regardless, I am posting from scenic Jerome, AZ which is a quaint town.

In anycase, read an article in The Economist on the way down here about how the Chinese a couple months back decided to blow up a satellite.

I remember the American response, according to the media, that we were appalled and this was saber rattling and China just showing us that they could knock out our satellites, which would impair a fair amount of the military.

However, I found out the real reason for NASA's angst and that was in blowing up just one aging satellite the Chinese literally bolstered the amount of debris floating around which, when coming in contact with a rocket flying at mach 7, results in a fair amount of damage. Thus the chart which I found interesting;

In any case, will be back later in the week. Postings will be sparse.

The Captain is on vacation and will not be making lot's of posts as I'm hiking out in the wilderness and sleeping at waysides (as hotels cost money, and it is more economical). Plus I'm out in Arizona and this is a big state with a lot of open spaces where there is no internet access.

Regardless, I am posting from scenic Jerome, AZ which is a quaint town.

In anycase, read an article in The Economist on the way down here about how the Chinese a couple months back decided to blow up a satellite.

I remember the American response, according to the media, that we were appalled and this was saber rattling and China just showing us that they could knock out our satellites, which would impair a fair amount of the military.

However, I found out the real reason for NASA's angst and that was in blowing up just one aging satellite the Chinese literally bolstered the amount of debris floating around which, when coming in contact with a rocket flying at mach 7, results in a fair amount of damage. Thus the chart which I found interesting;

In any case, will be back later in the week. Postings will be sparse.

Monday, January 21, 2008

Interest Rates Should Go Down

Set aside the Fisher Formula and what have you and consider this. While the markets and the economy may be on the brink to head into recession, the silver lining, and it's a big one for it directly affects the forces causing today's havoc and headaches is that interest rates, short and long term, will go down. Lower interest rates mean increased demand for housing, which might not necessarily "save" the housing market, but certainly could make this spring at least "better" than it has been. Not to mention if rates decrease enough, a smaller "refinance boom" might occur as people take whatever steps they can to tighten their finances.

Regardless, sorry for the lack of posts, but it's that greatest time of the year;

Tax Season.

Regardless, sorry for the lack of posts, but it's that greatest time of the year;

Tax Season.

Friday, January 18, 2008

Operation Market Garden Hits the Financial World

In light of the stock market crashing, and Merrill Lynch and Citigroup posting losses and the economy on the precipice of recession, I thought it worthwhile to bring up an old post of mine.

Thursday, January 17, 2008

The Captain's Economic Advice

I shall bring up an old idea I had a while ago that if we really wanted to help America avoid a recession and put her back on track, the the most effective stimulus package would not be to cut taxes (though that wouldn't hurt) or increase government spending. It would be to make any paying down of your mortgage tax deductible.

CDO's might have some value and start trading again. Defaults would go down. Interest rates would go down. And the future solvency of America would improve.

But, as always with modern day America, that's unconventional! That won't work! It's too revolutionary! Why it's so simple, it's like a sales tax replacing an income tax! It just can't be done! It's like Obama winning the democratic nomination! Why, next thing you know women will be getting their husbands martini's, men will learn how to wear suits and buy flowers for their wives, and children will be forced to do their homework and get good grades! What you think this is some mythical place like 1940's America?

CDO's might have some value and start trading again. Defaults would go down. Interest rates would go down. And the future solvency of America would improve.

But, as always with modern day America, that's unconventional! That won't work! It's too revolutionary! Why it's so simple, it's like a sales tax replacing an income tax! It just can't be done! It's like Obama winning the democratic nomination! Why, next thing you know women will be getting their husbands martini's, men will learn how to wear suits and buy flowers for their wives, and children will be forced to do their homework and get good grades! What you think this is some mythical place like 1940's America?

You Can't Make This Up

I hope when I am dead at least I will leave this little blog as kind of a record of history of how things happened. But most importantly, when they inevitably do prove global warming to be a hoax, that these pictures will be used to historically document the idiocy of it all, along with Dotcom Mania, Beanie Babies and the hopes of the Minnesota Vikings winning a super bowl.

Giggity Giggity Over Stock Market Valuations

Housing was overvalued, we knew that....well some independent thinking younger folk knew that. Obviously not the higher ups at Wall Street's "elite" bulge bracket" who were paid multiple hundreds of millions of dollars in compensation to run America's largest financial institutions into the ground. But why rub salt into blue blooder's wounds?

In any case there is another asset bubble. I've always worried about what would happen when the Baby Boomers retire instead of contribute $60 billion per month in 401k contributions, instead started selling out of stocks and move to fixed income? But complicate that with the prospect of American companies losing money or at least not making as much money as they previously did and the stock market looks precipitously close to a crash.

Of course this has already started happening as the primary driver of American corporate profits has come to a stand still; property values and very loose, borderline charitable credit.

Alas why I like the chart provided by Professor Genius Robert Shiller who has measured the S&P 500's P/E ratio going back to 1881. The average multiple at which a stock's price trades above it's earnings is about 16.

Today its around 40% more its historical average. Though this chart does not include the market's follies in the past month, the market could still have a way to go before it gets back in line with historical trends.

But don't worry. They're TALKING about THINKING about CONTEMPLATING about PONDERING the CONCEPT of MAYBE implementing a THEORETICAL stimulus package in Washington.

Giggity, freaking, giggity.

In any case there is another asset bubble. I've always worried about what would happen when the Baby Boomers retire instead of contribute $60 billion per month in 401k contributions, instead started selling out of stocks and move to fixed income? But complicate that with the prospect of American companies losing money or at least not making as much money as they previously did and the stock market looks precipitously close to a crash.

Of course this has already started happening as the primary driver of American corporate profits has come to a stand still; property values and very loose, borderline charitable credit.

Alas why I like the chart provided by Professor Genius Robert Shiller who has measured the S&P 500's P/E ratio going back to 1881. The average multiple at which a stock's price trades above it's earnings is about 16.

Today its around 40% more its historical average. Though this chart does not include the market's follies in the past month, the market could still have a way to go before it gets back in line with historical trends.

But don't worry. They're TALKING about THINKING about CONTEMPLATING about PONDERING the CONCEPT of MAYBE implementing a THEORETICAL stimulus package in Washington.

Giggity, freaking, giggity.

{kind=link}

Tuesday, January 15, 2008

Mexican Work Ethic

If you don't work you don't eat. Very simple concept. Because if everybody watches too much 90210 or it's current day "I was young in 1991 but now I'm approaching 40 but still want to feel young" incarnation "The Cashmier Club" or whatever the heck it's called, then you think wealth, food, shelter, clothing and SUV's grow on trees and are naturally supplied by the government or a rich husband. And though I am against illegal immigration and am the first to support the minute men, I will in economic intellectual honesty tip my hat to the work ethic of Mexicans, particularly the youth. For you see, if you want to know who will be taking care of you in old age and paying those social security contributions not to mention leading the country and being the best indicator to future economic growth you have to look at youth.

My only question is what the hell is up with Poland???? Good lord, didn't you learn your experiences with communism that should make you grateful to go out and kick a$$ and take names and work? What are you waiting for????

My only question is what the hell is up with Poland???? Good lord, didn't you learn your experiences with communism that should make you grateful to go out and kick a$$ and take names and work? What are you waiting for????

Captain for President 2012

I have this buddy Arturo. He says that if I ever run for president he wants to be my campaign manager for the sole reason he wants credit to the slogan;

"Shut the F#ck Up. I know What I'm Doing. Vote The Captain as President 2012."

So for my good buddy Arturo I present you this.

"Shut the F#ck Up. I know What I'm Doing. Vote The Captain as President 2012."

So for my good buddy Arturo I present you this.

Monday, January 14, 2008

The R Word

I speak now with the youth of this world and none of them, American or immigrant know of Bugs Bunny. Seriously I dated this 19 year old girl (lord knows why) and she didn't know anything about Bugs Bunny...nor other things. Thus, to revive this long lost icon I shall plagiarize the song from a Bugs Bunny cartoon "The Rabbits are Coming; Hurray Hurray!"

Recession is coming hurray hurray

Recession is coming hurray hurray

The bankers will suffer hurray hurray

Til the taxpayers bail them out hurray hurray

And they'll go back to playing golf hurray hurray

And driving their beamers hurray hurray

And dating 25 year old bimbos hurray hurray

And bragging about their hallow success hurray hurray

Till I get a terminally ill disease hurray hurray

And hunt them down and kill them hurray hurray

Recession is coming hurray hurray

Recession is coming hurray hurray

The bankers will suffer hurray hurray

Til the taxpayers bail them out hurray hurray

And they'll go back to playing golf hurray hurray

And driving their beamers hurray hurray

And dating 25 year old bimbos hurray hurray

And bragging about their hallow success hurray hurray

Till I get a terminally ill disease hurray hurray

And hunt them down and kill them hurray hurray

The Balance of Power Has Shifted

Ouch. Shot down like a young idealistic 17 year old American male that still believes in chivalry.

Saturday, January 12, 2008

Aaron Clarey

People have been asking what I look like. This is me as a professional.

This is me as a non-professional on St. Patrick's Day....well that IS being a "professional" on St. Patrick's Day, but not in the traditional sense of the word.

Friday, January 11, 2008

The Thin Red Line

I was cleaning out the Captain's Cave and came across the OECD Pocketbook that I got for free when I filled out a survey and while paging through it came across one of my favorite charts that shows both PUBLIC and PRIVATE spending on health care per person in the OECD.

And what it shows is what I've been saying for, I don't know, five, six years. That the US government already spends more than the majority of European governments per person on health care. That if the left has an argument it's NOT to spend MORE money on health care, but to streamline the current system. Thus the red line to show you the case. In any case enjoy the weekend.

And what it shows is what I've been saying for, I don't know, five, six years. That the US government already spends more than the majority of European governments per person on health care. That if the left has an argument it's NOT to spend MORE money on health care, but to streamline the current system. Thus the red line to show you the case. In any case enjoy the weekend.

Wednesday, January 09, 2008

Yet Another Reason Why It's Not "Big Oil"

I like this chart because it shows you two things;

1. That part of the reason gas is so expensive here in the US isn't so much the scarcity of oil (though that has its effect too), but the fact that the US dollar has lost so much of its value that it takes that many more dollars to buy a barrel of oil. Note compared to the Euro oil is not that expensive. Alas there is a price to pay to think that you can just borrow to live and not produce.

2. It compares three currencies (lest you have forgotten that gold was at one time a currency). If we were to be on the gold standard then oil really wouldn't be any more expensive than it was in 2000.

Now you can go ahead and blame the Fed for debasing the currency and blame Alan Greenspan because you have a headache, but the truth is that what really gives a currency it's value today is the wealth that you can buy with it.

For example I cannot go to Malaysia with US dollars and buy stuff. I have to convert it into the Malaysian currency, the Ringgit . Thus the only thing you can buy with US dollars is the stuff sold in the US. Therefore the value of the dollar depends on how much stuff Americans produce, not just "because the government says it has value." And if Americans insist on borrowing money from their homes to go and buy a big screen HDTV made in China, they are not producing anything of value here and therefore debasing the currency.

So if you want cheaper gas, cheaper imports in general, not to mention a whole slew of benefits that could be attained by producing more and spending less, take a second job, start paying off your debts. Quit using your house as an ATM and become an old school American. Increase the value of the dollar.

1. That part of the reason gas is so expensive here in the US isn't so much the scarcity of oil (though that has its effect too), but the fact that the US dollar has lost so much of its value that it takes that many more dollars to buy a barrel of oil. Note compared to the Euro oil is not that expensive. Alas there is a price to pay to think that you can just borrow to live and not produce.

2. It compares three currencies (lest you have forgotten that gold was at one time a currency). If we were to be on the gold standard then oil really wouldn't be any more expensive than it was in 2000.

Now you can go ahead and blame the Fed for debasing the currency and blame Alan Greenspan because you have a headache, but the truth is that what really gives a currency it's value today is the wealth that you can buy with it.

For example I cannot go to Malaysia with US dollars and buy stuff. I have to convert it into the Malaysian currency, the Ringgit . Thus the only thing you can buy with US dollars is the stuff sold in the US. Therefore the value of the dollar depends on how much stuff Americans produce, not just "because the government says it has value." And if Americans insist on borrowing money from their homes to go and buy a big screen HDTV made in China, they are not producing anything of value here and therefore debasing the currency.

So if you want cheaper gas, cheaper imports in general, not to mention a whole slew of benefits that could be attained by producing more and spending less, take a second job, start paying off your debts. Quit using your house as an ATM and become an old school American. Increase the value of the dollar.

Tuesday, January 08, 2008

Shooting Themselves in the Foot

Look, I loathe democrats. Really I do. But when you see an underdog like Obama and somebody who really does represent change (what change that is I don't know, but it really is better than another 20 year bout of Clintonbushbushclinton) it's hard not to cheer for him. Plus having Hilary the opposite ticket makes it really easy to cheer for him. Regardless, can the foot soldiers of the democrat party take the time to muster an independent thought and vote for the right candidate?

So I will say it again, even though it is against my personal interests to say so.

If the democrats want to lose the presidential election (you know, the one that counts) nominate Hilary. She is unelectable. And I internally fight within myself to temper my desire to see Obama nominated even though it would result in the defeat of the Republican party, with my machiavellian ulterior motive to see Hilary win for it would guarantee a Republican victory.

That being said, at minimum, AT MINIMUM this contested race shows Hilary and the archiac 60's power structure behind her is waining and the day will come that the mantle will be passed.

So I will say it again, even though it is against my personal interests to say so.

If the democrats want to lose the presidential election (you know, the one that counts) nominate Hilary. She is unelectable. And I internally fight within myself to temper my desire to see Obama nominated even though it would result in the defeat of the Republican party, with my machiavellian ulterior motive to see Hilary win for it would guarantee a Republican victory.

That being said, at minimum, AT MINIMUM this contested race shows Hilary and the archiac 60's power structure behind her is waining and the day will come that the mantle will be passed.

We're Just Not Getting It

So I checked up on an old chart of mine that needed updating and that was what percent of the total mortgage were people taking additional cash out. Normally this amount hovered around 5% in the 1990's. Then the refinance boom and housing scandal occurred and people used their appreciating property values as a substitute for working for a living, driving this ratio up to about 30%.

Now one would think that with all the hubbub and hoola going on about the housing market and prices actually decreasing, we Americans would get it through our skulls that you just can't live off of perpetually increasing property prices and that inevitably we'd have to do what our forefathers did and that was work hard, thus driving this ratio down.

You would think.

And we wonder why the dollar is tanking.

Now one would think that with all the hubbub and hoola going on about the housing market and prices actually decreasing, we Americans would get it through our skulls that you just can't live off of perpetually increasing property prices and that inevitably we'd have to do what our forefathers did and that was work hard, thus driving this ratio down.

You would think.

And we wonder why the dollar is tanking.

Oh Yeah, That's Right, Young People Have the Right to Vote Too

Look, seriously, you can pass the torch to Gen X. It's alright. Besides, it's inevitable. Why not now. Early retirement is calling.

Monday, January 07, 2008

PPP is a Tricky Bastard

The idea that it doesn't matter how much money you make, but rather how much stuff that you can buy not only explains why "the government can't just print off more money" but also allows us to compare the true standards of living in different countries.

$5,000 here in the US may not be a lot, but in Indonesia it will get you pretty far.

Even locally you can see the purchasing power parity effect where a $50,000 salary will have you sitting pretty in Fargo, but have you dirt poor in New York City.

In any case, comparing cost of living adjustments in the US is one thing as the country is relatively homogeneous. But comparing standards of living in Ethiopia versus Britain presents a slightly more difficult problem. So it should be no surprise that when international entities like the IMF and World Bank revise their PPP adjustment ratios then large sways in standards of living and GDP's can occur between different countries. And such is the case in China.

Don't get me wrong. China still is by all official measures the second largest economy in the world. But when the World Bank updated their PPP exchange rates, it lobbed off 40% of China's RGDP.

Alas it seems it will be 2020 before China surpasses the US as the world's largest economy. not 2016 as I predicted.

$5,000 here in the US may not be a lot, but in Indonesia it will get you pretty far.

Even locally you can see the purchasing power parity effect where a $50,000 salary will have you sitting pretty in Fargo, but have you dirt poor in New York City.

In any case, comparing cost of living adjustments in the US is one thing as the country is relatively homogeneous. But comparing standards of living in Ethiopia versus Britain presents a slightly more difficult problem. So it should be no surprise that when international entities like the IMF and World Bank revise their PPP adjustment ratios then large sways in standards of living and GDP's can occur between different countries. And such is the case in China.

Don't get me wrong. China still is by all official measures the second largest economy in the world. But when the World Bank updated their PPP exchange rates, it lobbed off 40% of China's RGDP.

Alas it seems it will be 2020 before China surpasses the US as the world's largest economy. not 2016 as I predicted.

Sunday, January 06, 2008

Just Can't Get it Up

The savings rate I mean. We don't even have increasing asset prices and yet Americans still find to spend more than they make.

Saturday, January 05, 2008

And So It Begins

Unemployment came in higher than expected. And if you are to be a technical analyst about it, you'll notice that it is a RARE event where housing tanks to such a degree and the economy does NOT fall into recession.

When the recession starts, let's just remember to be intellectually and politically honest and not blame the recession (that should hit right around election time) on George Bush or the democrats in congress.

That being said, any body want to bet the presidential candidates aren't going to play the blame game?

When the recession starts, let's just remember to be intellectually and politically honest and not blame the recession (that should hit right around election time) on George Bush or the democrats in congress.

That being said, any body want to bet the presidential candidates aren't going to play the blame game?

Friday, January 04, 2008

When is Inflation Considered Inflation?

So they always separate "core" versus "nominal" inflation. The reason they do this is that two items (energy and food) are very volatile and can easily over or understate the "true" rate of inflation.

Normally the Fed and other economy watchers are only concerned about the core rate as they should be. However, the past five years or so the price of energy and food has consistently been higher than the "core" rate of inflation. And while energy and food are volatile, being persistently higher than the "core" rate, to the extent of five years makes me wonder if it really matters if you separate it out from "core" inflation. People still have to pay for gas. People still have to pay for food. And the more it costs, the lower standards of living are.

In any case the chart below shows nominal versus core inflation. Bar the last quarter you'll see nominal inflation consistently exceeding core inflation.

Normally the Fed and other economy watchers are only concerned about the core rate as they should be. However, the past five years or so the price of energy and food has consistently been higher than the "core" rate of inflation. And while energy and food are volatile, being persistently higher than the "core" rate, to the extent of five years makes me wonder if it really matters if you separate it out from "core" inflation. People still have to pay for gas. People still have to pay for food. And the more it costs, the lower standards of living are.

In any case the chart below shows nominal versus core inflation. Bar the last quarter you'll see nominal inflation consistently exceeding core inflation.

Happy Day!

I could not have asked for a better outcome.

Not only did Obama beat the ambulance chaser, but he also beat Hilary. And Hilary was down to third!

A glimmer of hope the hippies are losing power.

Not only did Obama beat the ambulance chaser, but he also beat Hilary. And Hilary was down to third!

A glimmer of hope the hippies are losing power.

Robert Mugabe's Recipe for Economic Success

Two parts wealth redistribution. One part mass printing of money. And you have a recipe that is the envy of all aspiring African nations.

Thursday, January 03, 2008

Holy Freaking Oil Batman

I knew the oil exporting countries of the world ad a positive balance of trade, but I didn't realize it amounted to nearly 20% GDP.

If there is any solace in this figure it will do two things;

1. Give progressively more capitalist sovereignties like Abu Dhabi the cash they need to westernize and modernize their economies thus fighting terrorism by providing a more stable economy.

2. Provide the cash they need to buy cheap foreign assets and maybe bolster stock markets and property prices here.

If there is any solace in this figure it will do two things;

1. Give progressively more capitalist sovereignties like Abu Dhabi the cash they need to westernize and modernize their economies thus fighting terrorism by providing a more stable economy.

2. Provide the cash they need to buy cheap foreign assets and maybe bolster stock markets and property prices here.

Tuesday, January 01, 2008

A Banking Christmas Carol Part 3

A continuation from part 2

When you are borrowing money, in essence what you are doing is going to a group of strangers that have deposited their life savings in a bank and asking them if you can have their money to pursue your own idea or venture. Of course you don’t go directly to the people, you go to the banks which are presumably the guardians and stewards of their money. But that still doesn’t change the fact you are effectively asking to borrow other people’s hard earned money.

Additionally, should you fail to generate the cash flow necessary to pay back the loan, it is ultimately the responsibility of the

You would think this would humble you enough to make extra certain that you would be able to pay back the loan. That you would do everything in your power to eliminate all the risks and uncertainties in the venture you’re about to embark on. That you would run projections, study the market, look at your competitors and have the most comprehensive and thorough business plan possible all in an attempt to make sure you could pay back the loan. And if you were a real estate developer, you would think one of the most basic, most simple and most important things you would do is measure the current level of supply and demand in the housing market to see how likely it was your houses would sell. That before you’d go and ask for $15 million of other people’s money you would make sure that you could sell those houses and pay them back in the first place.

You would think.

It was mid 2005 and my boss came into my office and put a file on my desk. It was a loan we had done for this real estate developer about a year ago and not only did he want to refinance the original loan but take out a new one for a new development he was proposing. The original loan was for a 36 unit town home development in a small suburb of

I immediately knew something was amiss for while I had heard of

Now basic 3rd grade mathematics would tell you something was wrong. For each town home would house roughly three to four people. This guy wanted to build 200 of them, suggesting roughly a 700 person increase in population. This implied that St. Peter’s population was going to grow by 23% in just one year.

When I brought this to the attention of my boss I was told that St. Peter was one of the fastest growing communities in

“Not to worry,” I was told. This developer was the 8th largest real estate developer in the state with over 20 years experience. Besides which he personally had over $30 million in net worth and could easily guarantee the loan. So it might take a little while longer to sell those town homes than previously expected. So what!? He could afford it!

A year later his company had gone under and the two developments had cumulatively sold a paltry 11 town homes. The banks had taken a large hit and he was no longer the 8th largest real estate developer in the state.

The same story repeated itself a year later. This time I was driving to the town of

“Developments? What other developments?”

We spent the next hour driving around

Of course nobody was expecting

Nobody did their homework.

How stupid these real estate developers had to have been to not bother to at least estimate the demand for housing in these areas is beyond me. To not even bother to see how many other developments in the area were being planned or were under construction to gauge the level of supply. And to have the hubris and arrogance to go and ask for millions and millions of dollars of other peoples’ money to build something they literally had no idea whether it would sell or not was bordering criminal negligence. As much as I wanted to believe it was relegated to just these two developers, I had been in the business long enough to know this was the norm. For in just two short months, the same situation repeated itself again.

This time I received a request for a $6 million loan to build (what else?) town homes. This was early 2007 when the housing crash was in full swing and there was already a glut of housing on the market. Even in a housing slump projects like this were doable, but it placed an incredible amount of importance on the pricing of the town homes. If priced too high, they wouldn’t sell. They had to not only be priced at the market, but probably below the market if they were to sell in any reasonable length of time.

So I drove out to the site where the town homes were going to be built to get a feel for the neighborhood and an idea of what kind of price they would command.

I looked to my east and saw a sea of town homes across the highway.

I looked to my north and saw a sea of town homes across the other highway.

But when I looked to the south I saw a gas station…nestled within a sea of town homes across the highway.

As far as the eye could see there were town homes.

So I drove through these developments and counted no less than 27 town homes that were for sale. When I returned to my office I conducted my own little market study, pulled the market data for the area and found that there were actually 47 town homes for sale in the area and the pricing for the average town home was around $120 per square foot (they price on a per square foot basis so you can compare prices of different sized properties).

“Surely,” I opined to myself, “the men asking to borrow $6 million of other peoples’ hard earned money have conducted similar such research and their pricing will be slightly below $120 per square foot.” “Surely” I postulated, “the men asking to borrow $6 million of other peoples’ hard earned money have conducted similar such research and are fully aware there are already 47 similar town homes for sale in the immediate area.”

Surely indeed. For when I looked at their proposed town homes, their prices and their square footage, their pricing came in at $172 per square foot. In other words, they had overpriced their town homes by 43%. If the average town home was selling for $200,000 they would charge $286,000.

Naturally I figured I must have missed something. If my figures differed by 5-10% in pricing, then it was likely they were just greedy and slightly over pricing their units and could be bargained down. But 43% suggested to me I had missed something completely. Perhaps these town homes were particularly special. Perhaps these town homes came with a built in Jacuzzi or had their own private vineyard. Perhaps a free F-16 fighter plane came with the purchase of a new town home. Or perhaps there was a squad of cheerleaders that would cheer you on as you parked your car, watered your grass and did other mundane tasks. And sure enough there was. After talking to the banker who brought me the deal, I found out these town homes would have access to a clubhouse. And this clubhouse not only had a pool but also had…

conference rooms!

No Jacuzzi.

No personal F-16 fighter plane.

Not even my own personal squad of cheerleaders.

No, just a lousy pool and some conference rooms in a clubhouse, and it would cost me an extra 43%.

Obviously these town homes would not sell. Obviously, these men had not done their homework. Obviously the bank would lose its money on this loan.

However there was good news. This loan differed from the other two in that this loan hadn’t been made yet, it was just a proposal. Meaning this loan and the problems that would come with it could thankfully be avoided. All the bank had to do was turn it down. You would think that it would just be a matter then of showing management the 43% overpricing of the town homes, not to mention the already existing 47 town homes that were already on the market, and the bank would promptly decline the loan.

You would think.

For the ensuing battle was more lengthy and contested than the Battle of Somme. On one side was the banker and the broker who brought this deal to our bank. On the other side was myself and all the research I had done. The banker contested and questioned every number and statistic I had. He made me show him where I got the data and how I pulled it thinking somehow I had a bias or vendetta against him and was trying to sabotage his career. Upon satisfying that request the broker then pulled his own “market study.” And surprise, surprise, the broker (who coincidentally was vested in a 1% commission should this deal go through) found that the town homes were “fairly” priced and that although 47 other town homes may be for sale in the area, they were not comparable to the larger, more “luxurious” town homes that were proposed.

True, the proposed town homes may be superior, but I showed them that my pricing had been done on a per square foot basis, which bypassed the need to find similarly “luxurious” comparable town homes. I also pointed out that even if the proposed town homes were more luxurious it didn’t warrant a staggering 43% premium over similarly sized town homes. Pushing the limits (and perhaps a bit smugly) I pointed out his study consisted of cherry picked town homes from neighborhoods that were in more affluent zip codes and picturesque, which then begat accusations of questioning his integrity and the use of the hurtful epithet, “young punk.”

Regardless, the biggest point of contention I came to find out wasn’t the location, the pricing or the current supply of housing, but rather the club house. The banker, visibly frustrated now said, “Look, you are completely ignoring the largest selling point of this development and that is the club house! What about the club house!?”

I thought to myself, “You have got to be kidding me?”

Six hours arguing over pricing per square foot, valuation techniques, comparables, housing inventory and zip codes and I come to find out that their whole argument, their whole reasoning for a 43% premium in pricing, their whole rationale for lending out $6 million of other peoples’ hard earned money was that stupid club house.

“What about it?” I asked.

“It’s a really great club house.”

And that’s when I realized that I was not dealing with rational people. No matter what I would say, they would still argue for the funding of this loan.

The land could be sitting on an old nuclear waste dump.

“But it’s got a club house.”

The land could border the tarmac to the international airport.

“But it’s got a club house.”

The land could buttress an active volcano, erupting at this very moment.

“But it’s got a club house.”

Opting to waste no more time I said, “Fine, let’s submit it for approval, see what the higher ups think.”

Thankfully in the end cooler heads prevailed and the loan was declined, but what was most disturbing about this episode was just how close this loan got to being approved. The most basic and simple common sense would dictate this loan be thrown out the window immediately. But the political pressure to make sales quotas was so high that management insisted we explore every possible way to make the deal happen, resulting in myself, the banker and various members of management wasting nearly 20 labor hours on something that should have taken no more than 20 minutes.

Sadly, while this particular development may have had a happy ending, the truth is the majority of real estate developments were never turned down, no matter how bad they were. At every bank I worked at and across the industry the story was the same. Real estate development deals that had little to no hope of being repaid were being made left and right. As long as somebody owned the land and had put together some nifty blue prints and an “artist’s conception” of what the finished town homes would look like, they were approved. And as long as the appraisal, no matter how inflated of bogus, showed a high enough value, they were approved. In my entire banking career I had seen no more than four real estate development deals turned down and all of this in the face of growing and damning evidence that a historic glut was forming.

What is potentially going to be the largest irony in the entire housing scandal, the secret that nobody is going to let you in on is that these deals, and to a large extent, the entirety of the housing crisis could have largely been avoided had the banking industry required one simple thing;

Absorption studies.

Absorption studies are simple reports or formulas that calculate how much a local market can “absorb” in housing. You look at various variables including the increase in population, housing permits issued, jobs added to the area, etc., and infer how much demand versus supply there is for housing. From this you can deduce, rather accurately, how many new units of housing the area will need in the foreseeable future.

The only problem is despite their obvious use and value not once, NOT ONCE in my years in banking did I ever see an absorption study. I had heard of them. I had studied them. I even composed some myself to internally analyze some proposals we received. But after all my years working in the banking industry and literally hundreds of real estate development proposals I had seen, not one of them included an absorption study.

Had an absorption study been required of all real estate developments it would have immediately paralyzed the forces that were contributing to the housing bubble at their source. Not only would the housing crisis been averted, but hundreds, if not thousands of real estate developers would have avoided filing for bankruptcy. The study would have shown them, quite clearly, that there was already an excessive amount of housing in most markets, that their properties would not sell and that they would lose money. Their plans would be taken off the table and demand would be allowed to catch up to supply.

Furthermore scores of mortgage lenders would have avoided bankruptcy not to mention legions of employees and contractors related to the housing industry would have avoided being laid off altogether.

But the consequences for refusing something as simple as an absorption study go beyond the developers, mortgage lenders and their employees. There is also a severe consequence to the banks and society at large.

In continually approving real estate loans that had no hope of ever being paid back, the banks effectively did two things that undermined their future financial health.

One, they made bad loans. It naturally follows that if you make bad loans, you will have losses. The properties won’t sell, the developer will not be able to pay you back, and not only do you lose out on interest, but if and when the houses do sell, you’ll probably only get a fraction of the money you lent out. This has already begun to happen.

Two, they impaired their own collateral. In theory to lower their risk and ensure they don’t lose their money, banks require that you pledge your house or real estate as collateral. That way should you fail to make your payments, the bank can repossess your property, turn around, sell it, and get their money back. But because of the sheer volume of real estate deals that were being made, banks flooded the market with housing, driving the market value of their collateral down to the point it was worth less than what was owed on it. So even if the banks did repossess these developments and try to sell them it is unlikely they’d ever recoup the full amount they loaned out.

These two things combined pose a serious threat to the banking industry. Because of the business they’re in, banks are naturally highly leveraged, meaning they have a lot of debt and very little equity. And it doesn’t take a lot in losses to wipe out the equity they have and send them into bankruptcy. Furthermore, as property prices drop and the banks repossess their failed real estate developments, the value of their collateral drops as well. This decreases the value of their assets, but does not change the value of their liabilities, forcing them to write off some or part of their loans, further eroding their net worth.

The end result is that many banks are facing the very real and increased prospect of bankruptcy. Unable to recoup the money they lent out, some banks will have to admit they do not have the money to honor and fund the deposits of all of their customers. Normally in the past this would have triggered a bank panic, people would have rushed to their local bank to get what money of theirs they could. But we no longer have bank panics because through various governmental entities, your deposits are guaranteed by the

By recklessly and irresponsibly lending money to questionable real estate developers various banks have pushed themselves to the brink of bankruptcy and in doing so have dramatically increased the chance of a government bailout. And what is particularly appalling is how these loans ever got made in the first place. It is inexcusable that bankers would advance the funds to these developments with absolutely no clue as to whether or not these developments would sell. It is unforgivable that with absolutely no absorption study, how they found nothing wrong with being so free with other people’s money to the tune of $8, $10 or even $15 million. And because of such stupidity it really forces one to think whether they consciously knew what they were doing and were just in it for the commission, or if they truly were that inconceivably stupid. Regardless of whether it was criminality or stupidity, it’s the taxpayer that will pay for their mistakes.

Of course the question is just how much are these mistakes going to cost the taxpayer? The last time renegade bankers ran unchecked was during the Savings and Loan crisis in the late 1980’s. That scandal cost the

Poor taxpayer just can’t get a break.

Subscribe to:

Posts (Atom)