SWPL exposes the fake, shallow tastes of either faux intellectually elitists or the brain-dead, automotonic herds and delivers to them the mockery and insult they so richly deserve.

For example - "Grad School." HOW GREAT IS THAT? You have some idiot that chose an undergrad degree that was so worthless, they go back for MORE of the same. In reality they are an idiot, BUT, because they have a masters in "fillintheblankhere" they think they're smart.

Or for the "brain-dead herd of lemmings" crowd - Professional sports. Again, how great is that? You have some idiot whose entire LIFE'S WORTH is based on whether or not one group of big guys throws the ball better than another group of big guys, discernible only through the color of the jerseys they wear. But, ohhhhhh wrath upon thee that dare insult the team that these morons have vested so much emotion, psychology and (foolishly) cash into simply because they wear the blue jersey!

But the ultimate kicker for SWPL is that these people are COMPLETELY oblivious to their idiocy. They don't realize they're being made fun of and most of them even think they're smarter than the average person (ever go to a "wine and cheese party?") They just plain don't get the fact that they are the butt of the joke.

Of course there's a problem. SWPL's are not some small group of people. They're the majority of people! And because this is a democracy and a relatively free market we genuinely intelligent people must suffer their idiocy.

For example television.

Um, please somebody explain to me why there are GLEE PARTIES?????

You want TV shows to throw parties over? Try Firefly. Try Cowboy Bebop. Try Venture Brothers. Try classical Bugs Bunny. Try Hogan's Heroes. Try Family Guy.

But GLEE????

Another example - the movie industry.

Why am I relegated to marginally good movies starring Jason Statham and cartoons like Despicable Me? Why is it for every "Saving Private Ryan" there's a score of "Eat PRay Love" or "Sex in the City 14" movies?

Going green anyone? Great, I get to pay higher gas prices, higher heating bills, higher electric costs all because it's fashionable to hate fossil fuels.

Even voting patterns.

Why do I have to face a 9+% unemployment rate and a doubling of the national debt?

Because Obama and socialism is just the latest SWPL craze.

Now I could go on, but hopefully I've managed to do two things;

1. Entertain the regular and genuinely intelligent readers that visit the ole Capposphere and

2. Anger and insult SWPL types to the point you might actually be listening now BECAUSE

I am going to lay down some super economic genius that is going to benefit EVERYBODY.

401k's are SWPL.

Yes, sorry to say, 401k's, 403b's, IRA's and whatever other retirement plan you've put together for yourself is SWPL.

Now, this is not to say saving for retirement is foolish, it's not. BUt what we have here is the "brain-dead herd SWPL" members flooding a market to the point purchasing stocks in the US just plain ain't worth it. Specifically, since the government gives tax breaks to invest in (primarily) stocks, what has happened is by default the government has ordained stocks as the defacto retirement vehicle.

Now I've pointed this out before and to great lengths. I also pointed it out probably 5 years ago and the article, though pure genius, went nowhere (because it wasn't SWPL). But now MAYBE, JUST MAYBE, people will listen to me.

This recent run up in the stock market from a DJIA of 7,000 to 12,000 has people very happy and excited. The problem is that the reason you buy stocks is NOT because you will sell them for more in the future. You buy them because of the profits they will (hopefully generate)

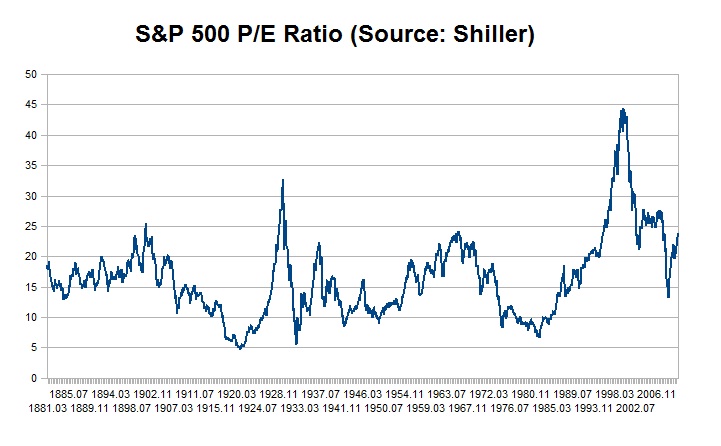

To measure this ratio of the price you pay to the profits you'll make, there is a thing called the P/E ratio. It takes the price of a stock and divides it by the earnings per share, showing you essentially how much you are paying in stock price for $1 in earnings. The higher, the worst the deal, the lower, the better.

Now the average has been since 1880 a ratio of roughly 15. Meaning you paid $15 in stock price for $1 in earnings. However during the peak of the Dotcom Bubble the P/E peaked at 45. That bubble burst, bringing the ratio down to 22, STILL NOT A GOOD DEAL.

But, ANOTHER SWPL fad came in - home ownership and condos and mcmansions!

THis drove the P/E ratio up again to 28, only until we found out the SWPL fad of buying a house you can't afford was not a sustainable economic behavior.

The Dow Jones dropped to 7,000 and with it the P/E ratio reached 14!

HURRAY!!!! LOOK AT THAT!!! THE STOCK MARKET IS ACCURATELY VALUED!!!!

NOT UNDERVALUED

ACCURATELY VALUED.

And so what do people do with stocks that are neither a steal nor overpriced, but just sanely valued?

A buying frenzy.

They drive the Dow Jones back up to 12,000 because SWPL's like to pay high stock prices for low earnings resulting in a P/E that is now around 24, implying a 30-40% overvaluation (denoted by the latest quick jump at the end of the chart).

Now Professor Robert Shiller, who is a real intellectual, not only provided this information, but logically concluded stocks are now overvalued again.

But ohhhhhh, my goodness! The SWPL's don't like that! They want stock bubbles! They want happy fuzzies for everyone! They want unicorn 401k's where you never have to work and solely rely on forever increasing asset prices to pay for your retirement. And they go out of their way to find a rationale or reason to continue living in SWPL Land.

Well, there's just one more problem with that guys.

See, while arguments can be made about whether you use earnings, EBIT, EBITDA and other things that aren't the bottom line, ultimate what drives stock prices are DIVIDENDS.

Because (and here's the economic lesson of the day), it is the only real cash flow a stock generates.

Oh, sure, you may sell the stock to another person generating a capital gain. But that didn't come from the stock. It came from another person. And the only reason that person paid you money for that stock is why?

Because the only thing a stock really generates is dividends.

And it is here, the only one TRUE cash flow that makes it to the stock holder and the only one TRUE cash flow that provides a stock with value that the situation is dire.

Below is the "dividend yield" for the S&P 500. This mathematically is the dividend per share divided by the price per share. In other words the rate of return you can expect from dividends.

And while the history of the dividend yield shows a rough average of about 5%, notice the general trend downward?

It reached a low back in the Dotcom bubble of 1.8%. Wow, that's a GREAT return! Let me get my checkbook out!

Of course there was a dose of sanity when the stock market collapsed this last time around, driving the dividend yield up to a whopping 3%.

But oh no. We can't have that! That's not SWPL! SWPL's like over valued stocks! We don't want any of those icky yuck gross dividends! And so with the reinflation of the stock market bubble the Dow Jones magically doubled in 2 1/2 years with no real economic growth, no real improvement in our economic future, sending the dividend yield back to 2%.

Now economists can go ahead and pull out their hair (like I did) about why the American public just plain doesn't get it and keeps on investing in overvalued markets. They can rack their brains asking, "did these people NOT just go through two massive bubbles??? Did they not learn their lesson? How did they DOUBLE the value of the stock market when the economy is in such dire shape and there's really no economic hope for the future?" But they will simply increase their blood pressure.

For there is no "logical" or "sane" reason these bubbles persistently and constantly form. It's much simpler. It's the same thing that causes people to make "going green" a hobby. It's the same thing that sends millions of people to fork over $10 a ticket to see mediocre movies. It's the same thing that makes people listen to something as boring as public radio.

It's SWPL!

Enjoy the decline!

23 comments:

How should someone invest money for retirement?

You're bang on with this one...

"COMPLETELY oblivious to their idiocy"

What gets me is that these people think everyone else is an idiot while they're acting the same way.

At least the folks who go to star trek conventions and dress up like Darth Vader or Chewbacca know they're geeks. The ones who go nuts over sports or sex in the city haven't got a clue.

Diversify into different asset classes.

Real estate (through either home or REIT's)

Commodities (though ETF's or commodity companies)

Stocks (just not in the US, preferably a place where the economy is growing and corporations are not villainized)

Fixed Income (again where people actually pay back their debts, not the US)

Education (not some fluffy crap liberal arts degree, but a skill or trade that people will pay for - auto repair, computers, HVAC, etc. Education and skills can NOT be taxed unless you convert it to income which means it's at your discretion how much you want to work).

Buy tools.

Share buy backs and debt reduction have the same value as dividends to shareholders. Instead of dividends the shareholder gets a capital gain since both of these tactics are accretive to share value. Share buy back less shares chasing the same market value. Less debt = more equity

Boomers saving for their retirement helped cause the bubble, and now that boomers are starting to retire and live of their investments the bubble will shrivel. Dividend yields should go back up.

Is diversification SWPL too? Or would that make you stupid?

Football is an excellent game and a great form of entertainment. Glee is a great show, and although I don't like it myself it is clearly a respectable product. Diversification is the only way to invest, as it increases your expected value in the long run.

You made one good point; tax receipts for 401k's inflate the stock markets.

You have some good points, but confuse them with the SWPL theme.

I love how when you divide the DJI by the P/E ratio that number remains constant between when it was valued at 7000 and where it is now.

P/E ratio is not something I have looked at when investing or for that matter really understood, it's not something financial planners talk about or focus on. All my investments for the last ten years has been in the company I work for. The P/E this year is a ridiculous 2.2. It was at 1.3 during the boom and has tapered off. By next year it should be at 5, which is still amazing.

Why is it always Shiller that provides the useful data? Everybody else mumbles meaningless platitudes and garbage, while Shiller does the leg work to produce real data and real evidence to make proper decisions.

Keith M: You mean to tell me not only is your source of income tied to a single company (your job) but you've sunk your savings into the same company? Scary.

I don't even invest in the same market segment as my job, if my job is in jeopardy that means the entire sector will be hurting, so the time when I need my savings the most they will be worth the least.

Shiller has a measurement called Cyclically Adjusted P/E which uses the trailing 10 year's earnings as the divisor - this indicates how much the market is overpriced. CAPE indicates 38% over.

There's another measurement called Tobin's q-ratio - this one indicates the market is 63% overpriced.

check out:

http://thehardtrade.com/tag/cape

http://dshort.com/articles/SP-Composite-pe-ratios.html

OK, this is a bit dated, but it will introduce you to what is POSSIBLE. http://www.twitvid.com/RG9ZX

The recent equities upmove is all smoke and mirrors and seems to be due to manipulation, the injection of QE2 funds and the "Bernanke Put." It CANNOT be sustained. Reality will eventually prevail, but whether this will be a inflationary or deflationary crisis is a matter of debate.

Our experience is ALL during a fantasic exceptional 30 year time. Reversion to the mean (and overcorrection too) imply that a stock divident yield of at least 6%is likely. Well that is only 1/3 of the current valuation of DJIA 12,000, which implies DJIA 4,000, (lets call it 5,000 to be generous). But wait a minute, dividends may also be cut in half, then that means DJIA 2,500. WOW!

RIGHT, I'm just delusional.... maybe.... but it this is within the realm of historical normalacy.

Dividend yields are declining and that seems irrational. But the fact is, you have to put your money someplace. At the same time as yields are declining, so are interest rates. I agree that 45:1 P/E ratios are a sign of irrationality but we should expect that yields will slowly decline.

By the way, that's a good thing. Firstly, it's a sign of a well-run economy. Just as arbitrage is impossible in an efficient market, windfall gains won't happen in a market with healthy capital access. In the end, this means society allocates less of its reward to capital formation and hopefully more to labour and innovation.

-Pete E

Another point on 401-k's and IRA's that has led to America's lack of innovation.

Before 401K/IRA era, a person would work for a company and have his retirement savings at the local bank. Maybe he would own a few stocks and even bonds.

After so many years of the grind, he may recognize a better way of doing his job, a better product than his company is producing or may just be ready to venture out to test the entrepreneurial waters for himself.

This would require him putting his retirement savings on the line in the new venture.

This is a big decision for anyone. It is risky for him and his family because failure is a possibility. But this "all or nothing" spirit and willingness to accept the risk was the first differentiator of successful people and companies.

But flash forward to today where the majority of people have their savings in a 401K/IRA and the entrepreneur faces another obstacle. HUGE penalties on his start-up capital.

The government is discouraging you from touching that money until you are too old to care.

Of course, they allow you to take loans against it for everything but starting a business. If you want to go into more debt by buying a bigger house, sure, there are allowances for that. Want to get an MBA, sure, no problem - there's a loan for that. But don't use that MBA to start your own business with the same funds.

Innovation is a two-sided coin. One side is ideas and the other is capital to make it happen.

It should really be called "Stuff Liberal White People Like."

While I plead guilty to several of them, I don't guzzle that Flavor Aid.

BTW, there's also "Stuff Black People Like" and "Stuff Asian People Like" that are pretty funny.

Keith M: Ever hear of a company called Enron?

Charles G: A savings account at a bank would be a wonderful thing, if the Fed would quit manipulating interest rates! It's hard to save when the savings rate is 0.5% because loan rates are at 3%.

Hi Cap! I think that your link about the "Stocks, Bonds, and Investing! Oh My!!!" is wrong...

C'mon CC

Glee is the only TV show my entire family sits to watch together.

IndianaHomez

The point was 401K/IRA accounts penalizes entrepreneurship.

The point was not to suggest putting your money in a savings account.

Clear enough?

As for the 401K and investing part of this, the market valuation is always determined on a technical component based on fundamentals/measurements and also to varying degree a psychological component.

As long as one thoughtfully builds a strategy which acknowledges those two components, monitors the market regularly and has good diversification, I think that's ok.

But just blindly throwing money into the stock market, without monitoring what's happening and without proper diversification like many do is asking for trouble.

Worse, these are the same people who jump out of the market when it has already dropped and jump into the market long after it has recovered.

Oddly enough, while I stayed fully invested in my non-retirement stock portfolio and continued my 401K contributions during the stock plunge in 2007 and the subsequent rebound, some interesting things happened:

- my 401K has pretty much recovered,

- by continuing to invest in the 401K, I bought a lot of stock at a deep discount,

- I captured a lot of capital losses by making some simple mutual fund trades at the bottom of the market and can carry them over to offset future cap gains.

I've told people that 401k's and IRA's amount to little more than market day for slaves.

Millionaires in Congress, regardless of party, have the power to change how much I can contribute (it was $2k per year in 1999), and how much I get to keep should I be able to retire.

SWPL is very slavish.

Post a Comment